This is the third in a series of posts on the 2024 Budget. Today: higher education by the University of Melbourne’s Abigail Payne, director of the Melbourne Institute. Last Friday: early childhood care and education by the University of New England’s Marg Rogers, postdoctoral fellow at the Manna Institute Last Thursday: school funding by Curtin University’s Matthew P. Sinclair, a lecturer in education policy.

I approached this year’s budget with excitement and with trepidation.

Why excitement? This budget offered the potential to embrace some of the more positive insights from the Universities Accord Report. Trepidation? Would we see the government fail to address the more challenging aspects of working at a university in Australia.

I had hoped to write about the promise of renewed investment in research, in the financing of universities, and supporting the important role that universities play for progressing innovation and delivering solutions that will support strong economic growth for Australia.

Frankly not much was announced about any important investment that must be made to strengthen and invest in our universities.

A quick search on terms revealed that the term “student” appeared 109 times, higher education 27 times, university 27 times, VET 25 times, TAFE 7 times, science 35 times, and research 65 times. This blog will focus on the budget announcements for addressing enrolment and the servicing of debt.

Importance of Increasing Tertiary Education Attendance

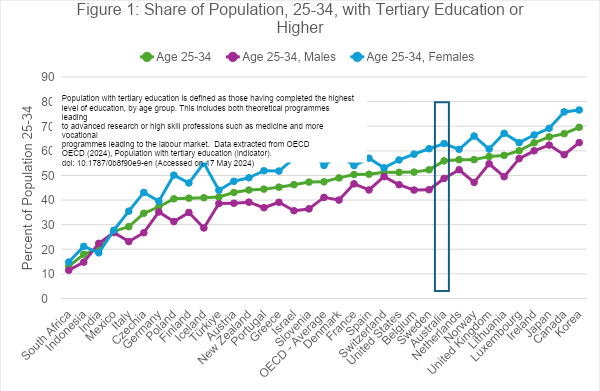

Let me start with the promising information. A goal of creating a highly skilled workforce that includes a tertiary attainment target of 80 percent by 2050. This is both laudable and ambitious. As Figure 1 depicts, Australia is ranked 10th amongst OECD countries for educational attainment (tertiary or higher) for individuals aged 25 to 34. The current rate for those living in Australia is 49 percent for men and is 63 percent for women.

Is increasing access to universities only about the money?

The budget also recognizes the importance of broadening access to encourage more underrepresented students to attend university. This importance will include a commitment for more needs-based funding. What this means for the budget is vague. And is the solution to achieving both an 80 percent target and broadening access simply about money? Increased financial commitments were announced in the budget: $1.1 billion over five years for expanded access and $350.3 million to expand access to free university courses.

Of course, money matters.

But research has shown, time and time again, the returns to further education are positive. That has not wavered over time. Why are we not observing high demand for university places?

Increasing educational attainment must include considerations: how we encourage students to prepare for pursuing these degrees; how we support our schools to deliver what is needed for success in university; and what we can do to support growth in the tertiary system. All that, while maintaining high standards to ensure graduating students are best prepared for opportunities that will require higher levels of skill and knowhow.

Addressing accumulated debt – will changing indexation solve the problem?

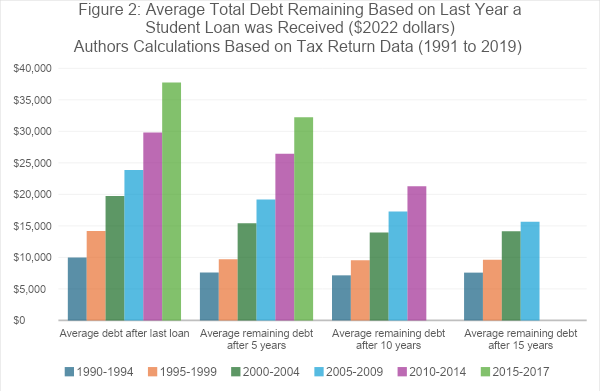

As has been well reported, as tuitions have risen, so has student debt. Figure 2 illustrates the dramatic increase in student debt based on tax data obtained from the Australian Tax Office, computed based on the year of the last observed loan for a student, reported in real ($2022) dollars. When HECS/HELP was introduced, the average accumulated debt at the end of schooling was $10,000 in today’s dollars. Today, the average is nearly $40,000. If we look at remaining debt after five, ten, and fifteen years (ignoring those who have fully repaid their loan), those with debt after ten years are still not making much of a dent in repaying the debt.

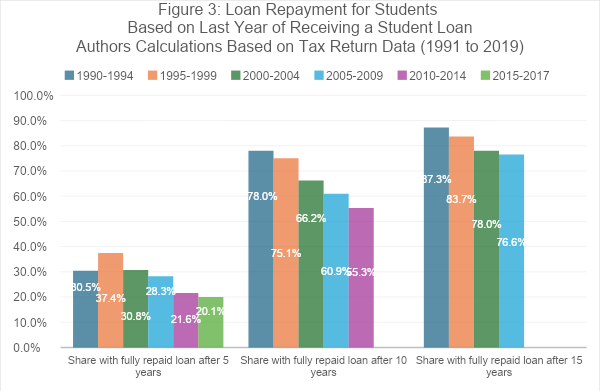

Increasing debt, and in more recent years, increasing effective interest on this debt has risen. This means that it is taking longer to repay debt. Figure 3 illustrates this fact. Using tax data and the loan information from the Australian Tax Office, we depict the share of students who have repaid their student loan debt after five, ten, and fifteen years, respectively, based on the year of the last year a loan was received. For example, if a student enrols in university in 2000 and takes out three years of loans between 2000 and 2002, the student is identified as having received her last year of loans in 2002.

What’s changed

When tuition was on the order of $2,000 (nominal) per year (1989 to 1995), approximately 30 percent of the students had repaid their loans within five years and 78 percent had repaid the loan within ten years. Fast forward to more recent periods: only 20 percent of students have repaid their loans within five years. Only 55 percent have repaid their loans within 10 years. As debt has increased so has the time to repay.

The budget has recognized the challenges of loan repayment. They have announced that the effective interest rate for these loans will change. The rate will be the lower of either the Consumer Price Index or the Wage Price Index. This use of different measures to capture “inflation” is welcomed.

Are the cuts to debt fair?

The Government has also indicated it will cut $3 billion in student debt, providing relief for those with existing debt. That’s welcome. But is it fair for those who no longer hold debt but paid off their loans in recent years? One should also consider the potential signal it serves regarding opportunities to pay off one’s loan faster than is required. And finally, what about those who have never held a loan but are struggling financially?

Confusions around tuition rates and debt repayment – does it cause a student to pause before enrolling?

Revisiting the question of how to increase participation in tertiary education, we should think about the role increasing debt plays on the decision to pursue a university degree. The income-contingent loan repayment scheme should be applauded for creating a structure to encourage participation while deferring payment for that participation.

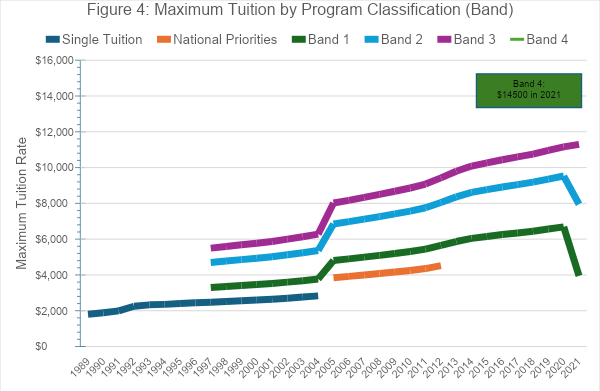

What started as a simple concept, however, has become convoluted. It may lead to confusion and a decision not to pursue further education. As Figure 4 illustrates, tuition has not only increased but there are differential tuition rates depending on the program of study. This aspect makes sense if the tuition rate reflects the cost of delivering the given program of study. This simple depiction of three or four rates, however, quickly gets confusing when a student pursues courses in different programs. Once enrolled, depending on course selection, a student can end up facing differential course fees, making it even more challenging to understand the total cost of a degree before enrolling in university.

Source: Parliamentary Library based on Department of Education, https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/rp2021/Chronologies/HigherEducation

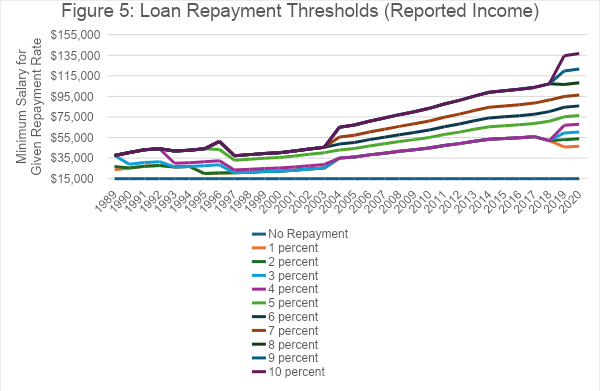

Potentially even more confusing for a student who wants to be fully informed before university registration is the repayment rates. The basic principle is that repayment is tied to earnings. With the minimum repayment amount equalling a percentage of one’s income.

But the percentage and thresholds vary across incomes and over time. Figure 5 depicts the minimum repayment rates. These have changed both with respect to what is owed as well as the income threshold for computing the amount owed. Given the repayment rates can adjust on a year to year basis, it would be very challenging to figure out at the time of university registration how long it might take to repay a student loan.

Source: Parliamentary Library based on Department of Education, https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/rp2021/Chronologies/HigherEducation

Encouraging greater participation and meeting 2050 targets

Encouraging greater participation in tertiary education must be more than making a proclamation. We can do more to invest in our institutions, to identify the factors that contribute to a decision to pursue a degree or diploma beyond secondary school, and to provide transparent mechanisms for capturing tuition and loan repayment. To encourage greater participation in tertiary education, information on costs and expectations for repayment should be clear and easy to understand.

Government has made a move towards reducing the costs associated with loan indexation. It has also provided temporary loan forgiveness, and is investing to promote greater access to university. But it should do more to embrace and address the challenges students AND universities face.

Abigail Payne is the Director & Ronald Henderson Professor at the Melbourne Institute: Applied Economic & Social Research at the University of Melbourne. Her research is wide- ranging and includes the effects of policy on educational outcomes, schooling transitions, gender differences, and student performance; the determinants of poverty and disadvantage and the mechanisms for reducing poverty; and charitable giving and the role played by nonprofits in service provision.

Australia may have already reached peak university enrollment, and that would be a good thing. More university students is not the best way to reach a 80% post secondary qualification level. The government made a subtle change in their target, which I suggested in my accord submission, to include vocational education in the 80%. A good way to reduce university fees is for students to attend TAFE first, & then those who feel they need university to get credit for their vocational studies. However, universities will need to lift their game with courses for students used to rapid, real world based courses.